Knowing you might not have time to watch our full webinars, we are pleased to continue our series of COVID-19 webinar summaries.

NB: This is an article from STR

In this latest edition, we talk performance in Asia Pacific.

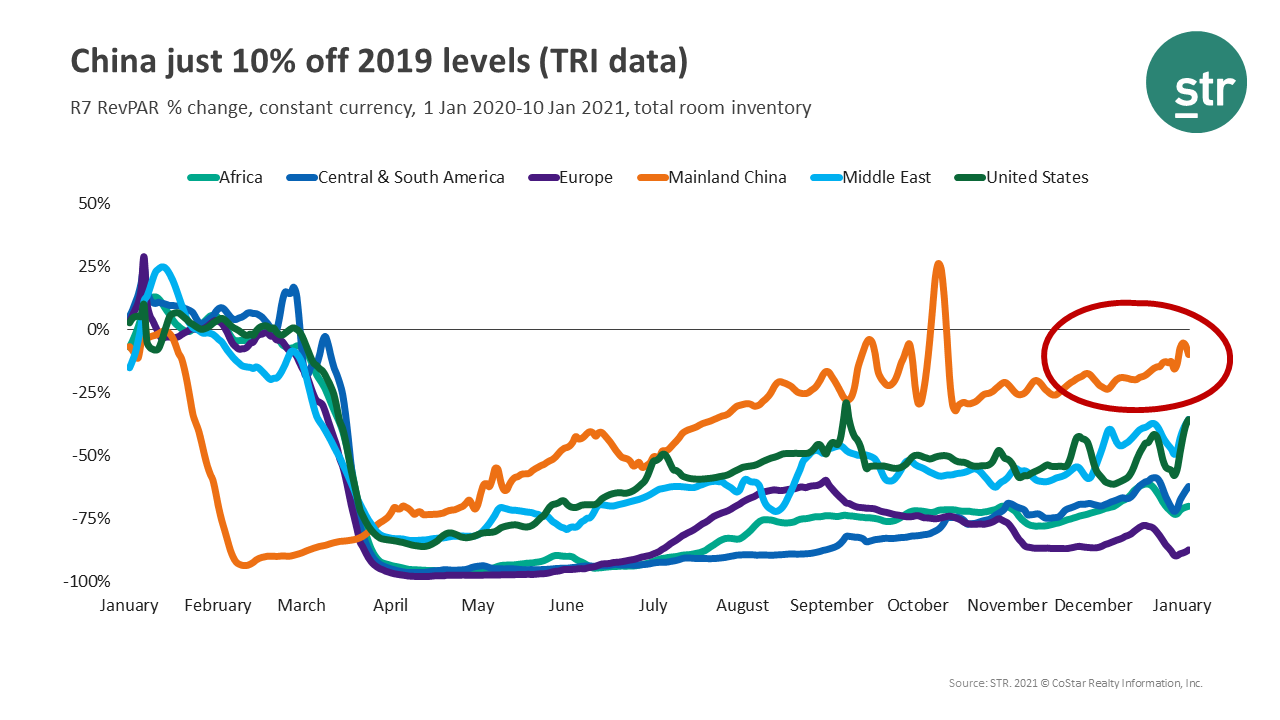

Mainland China just 10% off its pace

When using total-room-inventory (TRI) methodology, which excludes temporary closures due to the pandemic, Mainland China hotel RevPAR was just 10% behind its 2019 RevPAR levels. This was well ahead of other key regions around the world.

Subscribe to our weekly newsletter and stay up to date

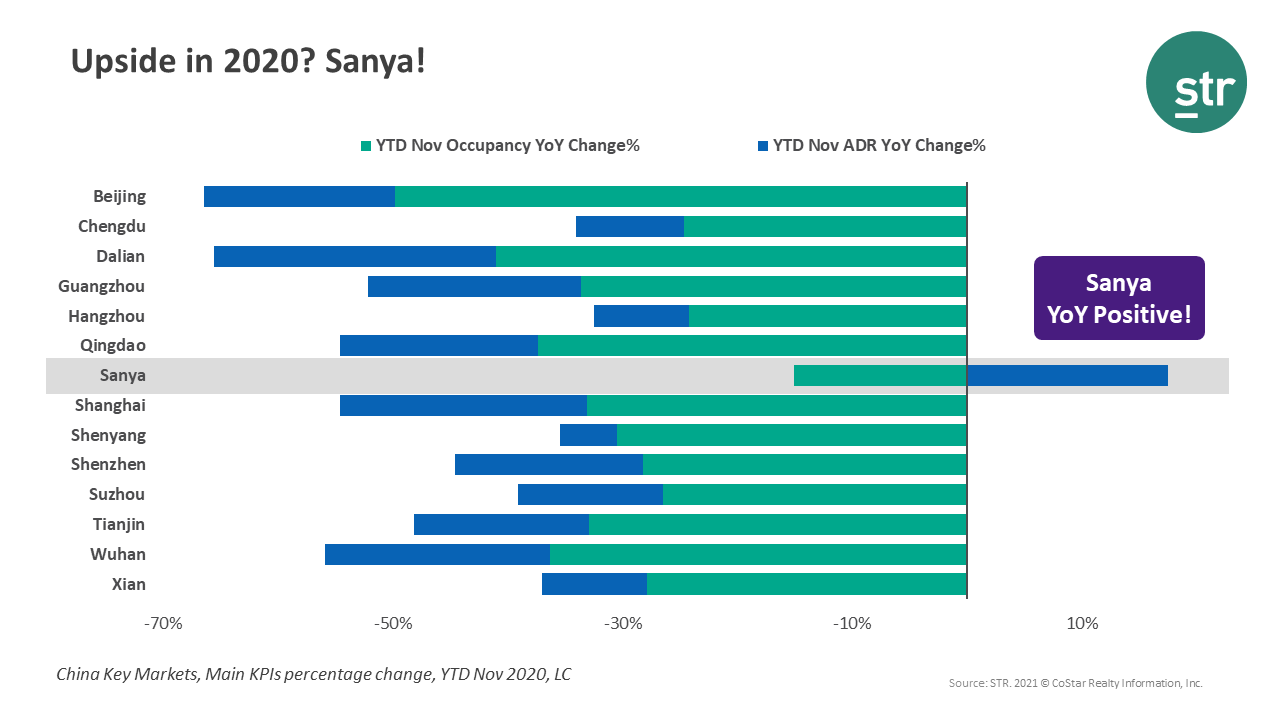

Sanya’s success

Sanya, in the Hainan province, was the only market in the region to record year-over-year growth in RevPAR. That growth was driven by ADR, which increased 4.7% in November for instance, thanks to leisure demand.Image

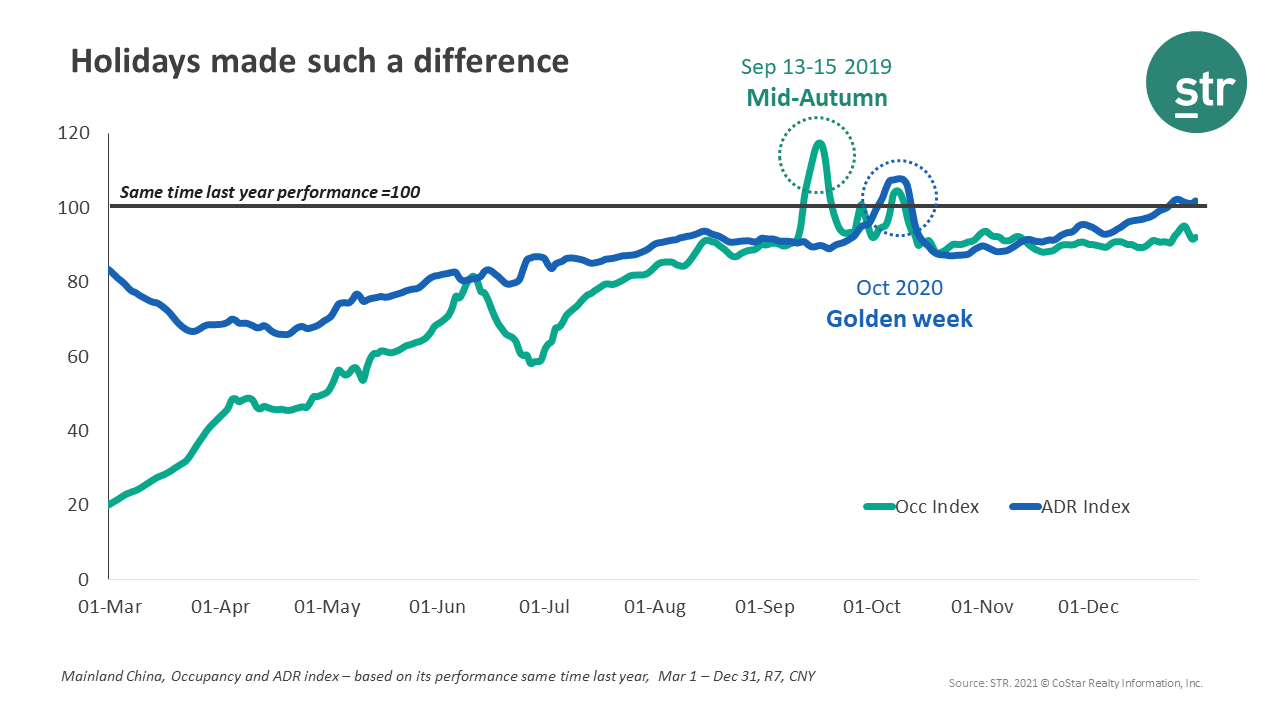

Holiday impact

The leisure boost witnessed during the summer extended to “Golden Week” for several markets in Mainland China. For some, ADR and occupancy levels rose higher than 2019 Golden Week comparables.Image

High-end average daily rate

All hotel classes in China have been impacted by the COVID-19 pandemic. However, the Luxury & Upper Upscale segment maintained ADR the best with just a 9.5% decrease. The next best comparison was Midscale % Economy (-11.2%).Image

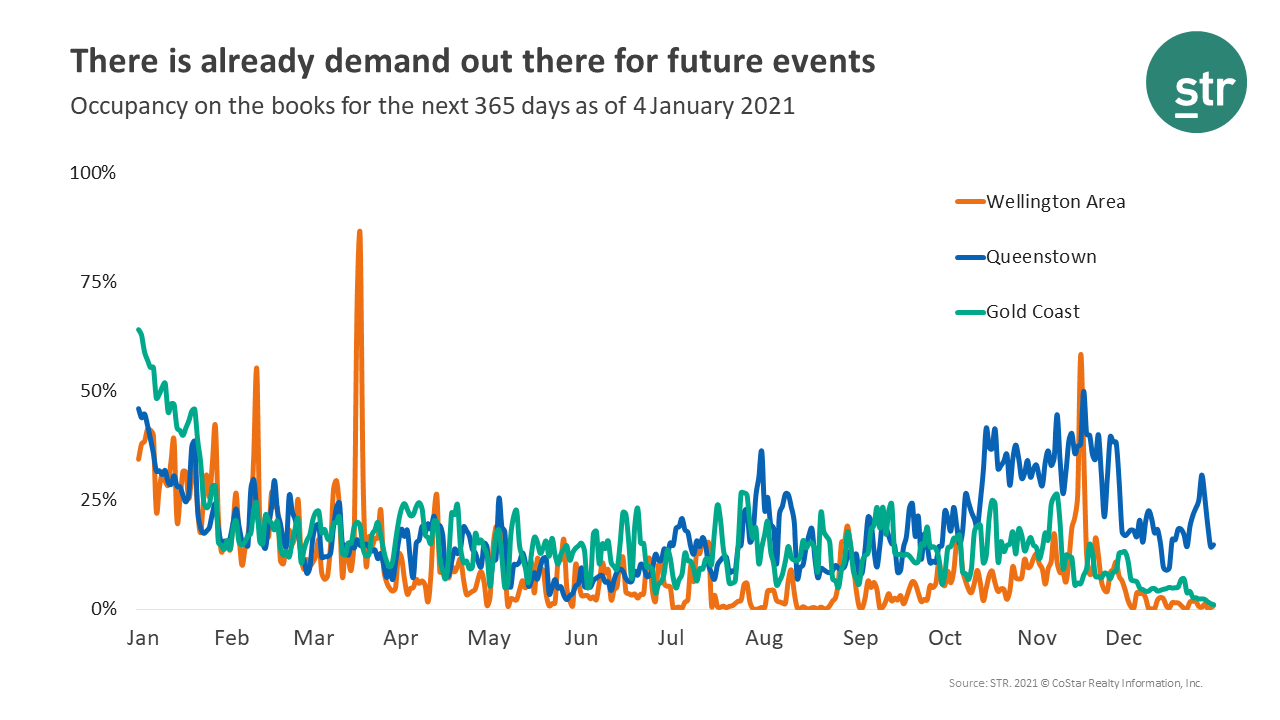

Forward-looking data shows events impact

The image below shows hotel occupancy on the books for the next 365 days (as of 4 January) in Wellington, Queenstown and the Gold Coast. Further insights are provided in the full webinar recording. Occupancy-on-the-books intelligence will help us all understand recovery and provide much-needed context. Those insights can be accessed for free when you submit your data.