At first glance, the hotel industry in the United States seems to be climbing back. Total revenue per available room (TRevPAR), gross operating profit per available room (GOPPAR), and payroll per available room (PayPAR) have all posted year-over-year gains.

NB: This is an article from HotStats

Subscribe to our weekly newsletter and stay up to date

But peel back the layers, adjust for inflation, and a different picture emerges – one where progress is slower, margins thinner, and true recovery still out of reach.

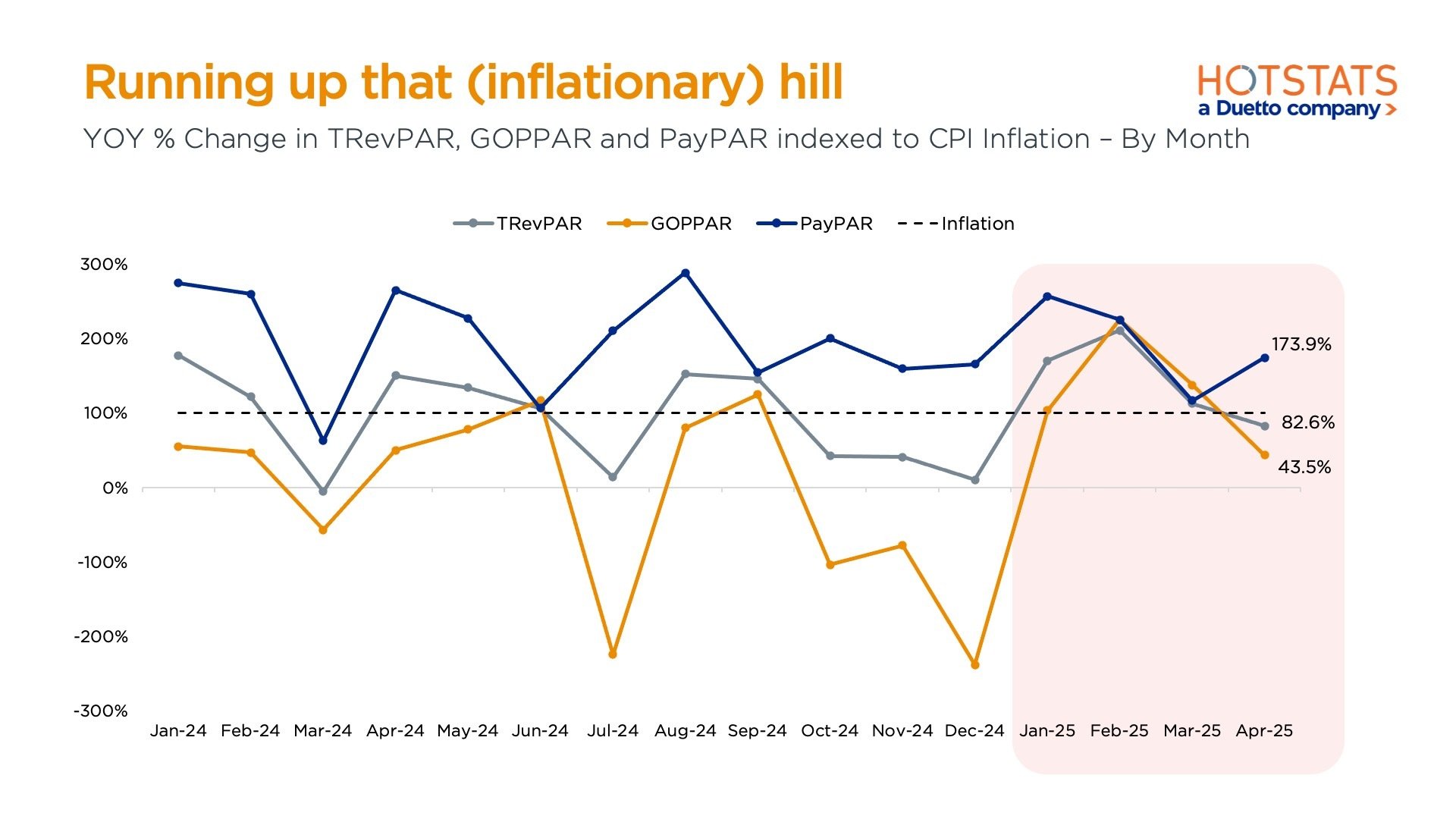

Figure 1

Hotels are hustling uphill. PayPAR is soaring, but GOPPAR and TRevPAR are still trailing inflation. April 2025 shows the gap—profits aren’t keeping pace with rising costs.

The latest HotStats data from April 2025 underscores a recurring truth in post-pandemic hospitality: nominal growth does not equal real recovery. Despite steady increases over the last few years, many U.S. hotels are still making less money in real terms than they did in 2019. When compared against the Consumer Price Index (CPI), which continues to trend upward, it becomes clear that inflation has silently eroded much of the apparent progress.

This is not just a statistical quirk. It’s a margin story. While revenue growth has been stubbornly slow to catch up to inflation, labor costs have charged ahead. Over the past year, payroll increases have outpaced revenue, putting immense pressure on operating profits. For hotels already operating on tight margins, this dynamic spells trouble. The result is a profitability landscape that may look stable at the surface, but underneath, is stretched thinner than it’s been in years.

“Margins are getting squeezed on both ends. You can’t raise rates fast enough to outpace inflation, says Resco, Director for Hospitality Intelligence in the Americas. “The inflation gap isn’t just academic – it’s something hoteliers feel every day on the P&L.”

That inflation gap is especially clear when comparing April 2025 to April 2019. Even as hotels report higher average daily rates and nominal revenues, GOPPAR has not kept pace with the increased cost base. What was once a resilient, if bruised, operating model is now being fundamentally tested.

Figure 2

Revenue is up, but margins are squeezed. In April 2025, GOPPAR and TRevPAR gains were far outpaced by inflation, while payroll costs climbed higher. Profit margins dipped slightly below 2019 levels, highlighting the ongoing pressure on hotel profitability.

Compounding the issue are the upcoming union negotiations in major U.S. cities – most notably in New York, Los Angeles, and Chicago. Any resulting wage increases will likely tip labor costs even higher, worsening the imbalance between top-line and bottom-line performance. In many cases, owners and operators are already struggling to manage service levels while keeping costs in check.