Signs late last week pointed to a negative performance impact from the hacking of the Colonial Pipeline and resulting gas shortages.

NB: This is an article from STR

Crisis averted, however, as U.S. hotel demand, occupancy, ADR and RevPAR all reached or were near pandemic-era highs. Further, all four measures hit pandemic highs when looking strictly at the weekend. Occupancy for the week averaged 59.1% or 56.4% on a total-room-inventory (TRI) basis, which accounts for temporarily closed hotels. That occupancy was the second- highest level of the past 62 weeks. Weekend occupancy was 73.6% (70.2 TRI), the highest level since Valentine’s Day weekend in 2020.

Subscribe to our weekly newsletter and stay up to date

After a fortnight of being flat or slightly falling, demand powered to its largest amount in more than a year, topping 22.4 million. Weekly room demand has been at 80% or more of 2019’s level for the past nine weeks. The largest weekly gains were seen in markets that tend to rely more on business travel, including Houston, Chicago, Los Angeles, New York, and Dallas. While these markets saw the largest week-on-week gains, New York and Chicago remain far from normal with this week’s demand at less than 50% of what was seen in 2019. Dallas, Houston, and Los Angeles are in a better position with 80% or more of the 2019 demand level realized last week. Overall, demand for the week increased by nearly one million room nights with 80% of all markets posting week-on-week growth. Thirteen states had demand at 95% or more of the level seen in 2019 with Texas and Florida, two of the three largest demand states, nearly at 2019 levels.

The surge in industry performance was widespread with the number of hotels with occupancy above 60% advancing to a new high. Despite the solid gains, there are still many hotels and markets suffering, especially large, convention hotels and markets dependent on group business. Overall, weekday occupancy for large urban hotels (300+ rooms) remained low (31.5%) and even lower in the Top 25 markets (30.9%). Seven markets reported weekly TRI occupancy under 45%, including San Francisco, New York, Washington, D.C. and Boston. Weekday occupancy for hotels that cater to business in top 25 urban locations continued to be weak at 45%, but up from the previous week.

Along with the solid gain in hotel demand, ADR also powered up and achieved a pandemic high (US$114) with the week-on-week increase (2.8%) the largest of the past eight weeks. ADR in the Top 25 Markets was also at a new high ($123), led by the weekend, up 4.4% from the previous week. Comparatively, ADR remains down about 15% as compared with 2019 on a nominal basis. The figure is higher when accounting for inflation.

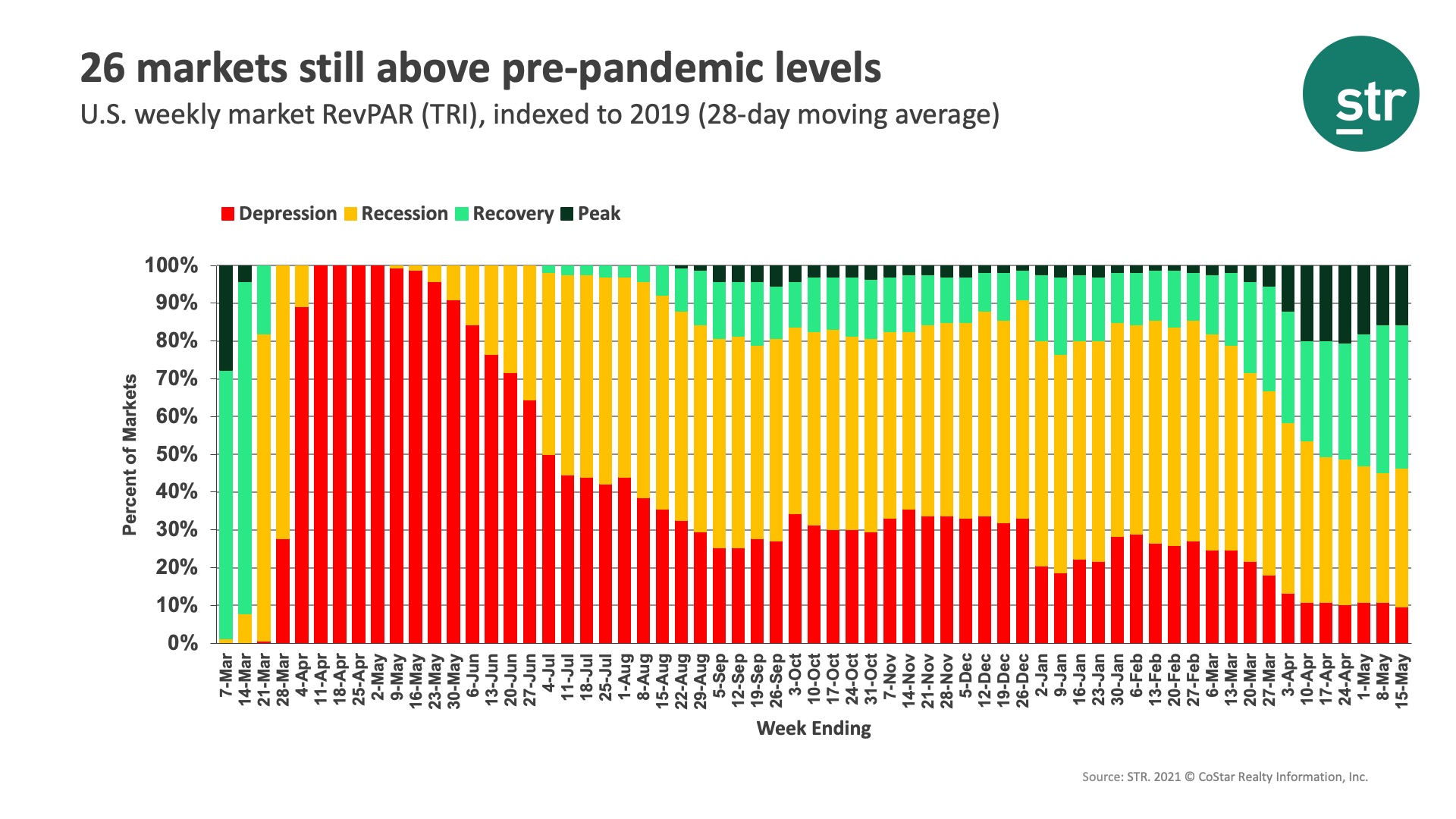

RevPAR increased 7% week over week and reached a 62-week high (TRI: US$64). The gain was even higher in the Top 25 (8%), especially over the weekend (14%) when RevPAR topped US$100 (TRI: US$93) for the first time since the start of the pandemic. The number of markets at “Recovery” or “Peak” fell slightly (from 91 to 89) with 26 markets still above their pre-pandemic comparables, led by the Florida Keys and Gatlinburg/Pigeon Forge. This week also saw a reduction in the number of markets in “Depression,” which fell to only 16, the lowest number so far. San Francisco continued to have the lowest RevPAR indexed to 2019, followed by New York, Boston, and Washington, D.C. RevPAR in these four markets remained under 30% of what it was in 2019. Overall, U.S. TRI RevPAR was at 68% of 2019’s level and its highest index of the past four weeks.

Outside the U.S., there was little to no change in the number of markets in “Depression” or “Recession” with 82% in one of those two categories. On a country level, China, Spain, and the U.K. saw the largest weekly demand gains, but hotel occupancy in the U.K. and Spain remained low at under 30%. China’s occupancy increased to 58% after falling in the previous week. Fifteen countries continued to have weekly occupancy below 10%.

This week’s U.S. performance was a bit of a surprise and the vanguard to the expected summer surge. While hotel demand will likely increase to levels not seen since summer 2019, we are mindful that many hotels remain in a weakened state with financial difficulties compounded with increasing labor issues. It will take time for the industry to heal, but we are hopeful that the performance we have seen recently will speed that process.