Hotels in North America and around the world are starting to look ahead to reopening their doors to guests.

NB: This is an article from Cendyn

As we speak, from the smallest independent boutiques to the largest global chains, properties are formulating strategies for operations, marketing, revenue management, and many other areas in the context of a post-COVID-19 environment.

Theories and forecasts abound as to what the actual ramp-up of business will resemble, with general agreement that companies should have plans in place for various scenarios. But looking at certain data now can help with understanding how and when supply will come back online and how demand will respond to hotel reopenings.

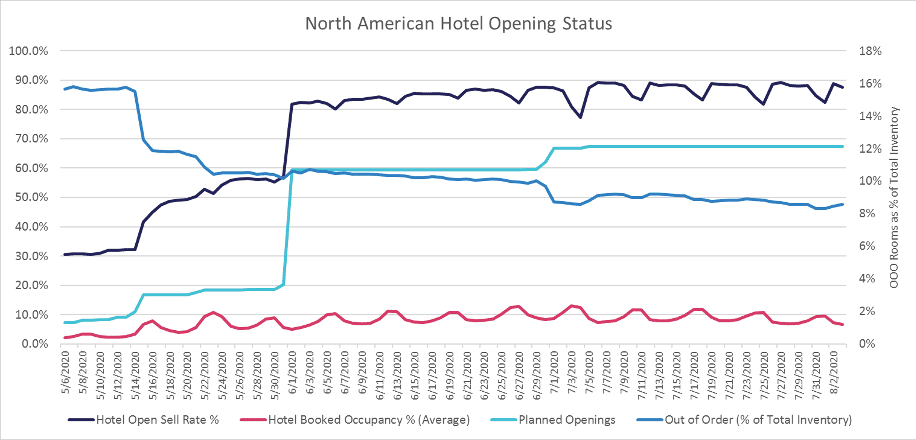

Three key data points are invaluable for identifying the ramp-up of supply, with their corresponding color-scheme from the chart above noted:

- Hotels that have rooms available for sale starting at some date in the future (dark blue)

- Hotels that have provided estimates of their reopening dates (turquoise)

- Out-of-order inventory across hotels and how hotels plan to phase it back in (light blue)

Slow ramp up to June 1, 2020 reopenings

Of the roughly 1,200 hotels for which rate data was available, as of the time of publication, about 30% show rooms available for sale for stay dates in the first half of May. We see a bit of a bump up mid-month, and by the end of May, 57% of these hotels as of now plan to be open. But the biggest jump happens on June 1st, where over 80% of hotels are selling for stay dates on this date or later. Beyond June 1st there is a gradual upward trend; it is interesting to note the small percentage of hotels that don’t appear to have selling rates available on weekends, which may imply a planned change in operational strategy for hotels that need to adhere to new standards of safety and cleanliness.

Selling ahead of anticipated reopening

The reopening timeframes that Cendyn’s customers are reporting to us closely mirror the trend in the ramp-up of for-sale dates. Key milestones for reopening appear to be in mid-May, June 1st, and July 1st, with June 1st again being the clear target date for the majority of the hotels. What is evident however is the gap between the percentage of hotels that are planning a certain open date and those that are actually selling. There are a few possible explanations for this; aside from differences in the populations across these datasets, hotels could still be selling ahead of anticipated opening dates in case they are ready to operate (somewhat of a “soft” reopening). There are also many hotels that have communicated to us that their opening dates are still “to be determined” – we did not include these in our count of open hotels, and many still may have selling rates out there as of certain dates.

How will sanitation protocol affect bookings?

Out-of-order rooms data is somewhat less reliable as many hotels may not be utilizing that PMS functionality during closures and will likely need to do a lot to stay on top of planning for a certain number of out-of-order rooms once they reopen. However, it will be interesting to track how inventory phases back in once hotels come back online, especially given possible constraints tied to health-related restrictions and other policies and procedures. For instance, many hotels are either required or are choosing to delay housekeeping services on vacant rooms anywhere from 24 to 72 hours after departure.

‘Wait and see’ approach

Despite the ramp-up in hotel openings over the next couple of months, it is evident that most prospective travelers may be taking a “wait and see” approach towards booking. Booked occupancy seems to trend consistently in the 10-13% range without a noticeable bump up that coincides with hotel openings. Depending on their market and business mix, operators should prepare for possible surges of pent-up demand once they officially reopen.

The entire situation of course is a very fluid one and hotels are constantly monitoring guidelines, restrictions, and demand with the goal of making the right economic decision on whether to reopen and when. Hotels will be faced with the unique challenge of limited inventory, rising costs per occupied room, and the need to fill enough rooms at some minimum price to justify “turning the lights back on” so to speak.

Read more articles from Cendyn

We recently spoke with Dan Skodol, VP of Data Science and Analytics at Cendyn around the exact topics touched on above. You can hear that interview here.